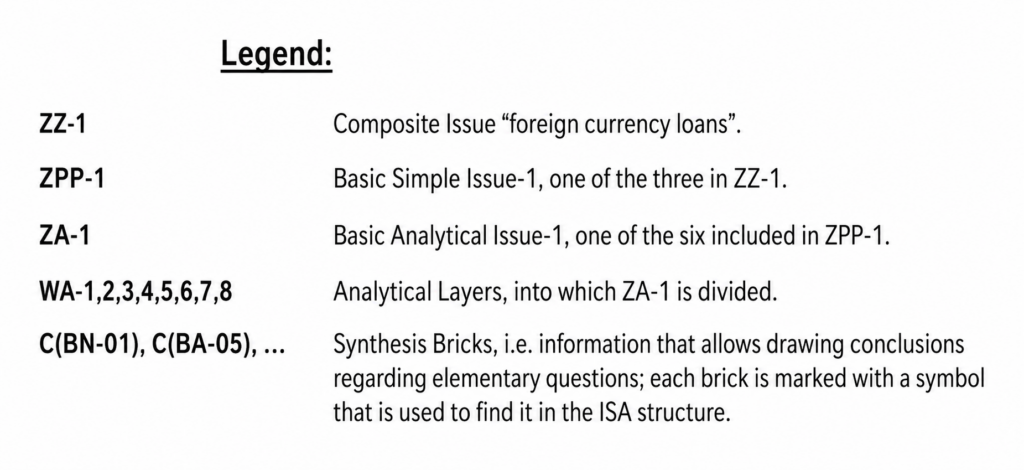

Introduction to Integrated Information on dual-currency loans

I built the model of the first Integrated Information around the issue of “pseudo-Swiss-franc loans” [CI1].

The analytical material for developing this issue was, for me, the content of public discourse.

The discourse that has been going on around this topic for more than a dozen years is multi-threaded, just as in the case of any other complex problem. The parties to the discourse analyze loan agreements in terms of fairness, comprehensibility, correctness, social justice, economic soundness, etc. Unfortunately, they do not separate the individual aspects into distinct analyses, but throw everything into one bag, which means that the scope of the analysis is not strictly defined but fluid. If the legal aspect is inconvenient for someone, they can shift to arguments from economics, ethics, social sciences, etc.

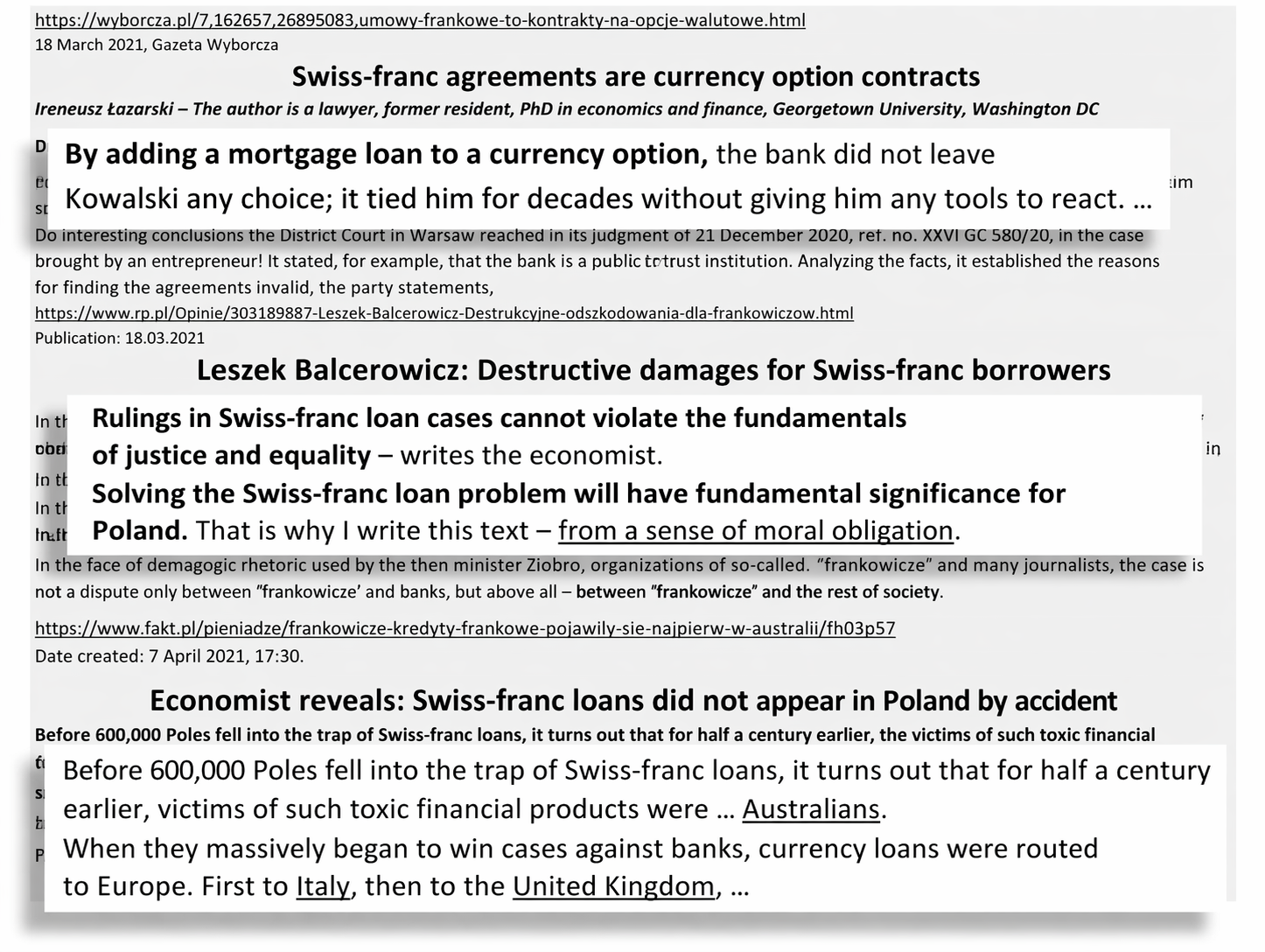

Here are examples of press headlines:

The characteristics of public discourse are multi-threadedness and chaos. The analyses cited within the discourse are neither consistent nor complete. On their basis, it is impossible to learn anything unambiguous; on the contrary, they often mislead the audience. By analyzing the content of the statements made by the parties to the discourse, however, one can precisely determine the general scope of the problem and the ways in which society perceives it. On this basis, a complete and ordered body of information can be created that will provide concrete knowledge when two conditions are met:

– we separate the individual aspects, that is, we examine economic soundness separately, legal correctness separately, the comprehensibility of the clauses for the consumer separately, etc.

– we consistently carry each analysis through to the end within separate, logically coherent scientific studies.

How will partial information be organized on the basis of the IAI model?

Pseudo-Swiss-franc loans are not only a legal issue, although legal issues are very important here.

However, analyses in the fields of psychology (e.g. the readability of a loan agreement, that is, the possibility of understanding the consequences resulting from its content), economics (e.g. a/currency trading, b/methods of determining exchange rates, c/contractual indexation, d/currency options, e/calculations of the so-called losses of the banking sector and analysis of their consequences), banking (e.g. a/fair examination of creditworthiness, b/calculations of loans: in PLN, in a foreign currency, and dual-currency loans), social sciences (e.g. a/the limits of the freedom to conclude loan agreements b/the three parties to the agreement, that is, the responsibility of state institutions for supervising the credit market c/the invalidation of a pseudo-Swiss-franc loan agreement in light of social justice), etc., are just as important here as law. From the perspective of law, one should examine consumer protection in EU regulations and in Polish legislation, because these two systems of protection are not the same. It is also worth recalling the origins of the creation of laws protecting ordinary people against abuses by corporations.

Dual-currency loans belong to those complex issues that are so complicated and extensive that, without organizing all the information related to them into a clear structure, it is impossible to draw correct conclusions, even if one is a professor of economics, of which there are many examples in press publications on this subject.

Instead of endlessly throwing arguments at one another drawn from different intersubjective realities, it would first be better to organize the arguments made by all sides of the public discourse and conduct separate logical analyses of them based on knowledge from several scientific disciplines. Only then can a clear picture of the whole issue emerge, from which unambiguous conclusions can be drawn. To do this, I first define the scope of the issue by determining the System of Necessary Reference Points. I then determine the Core Aspects for analyzing this problem.

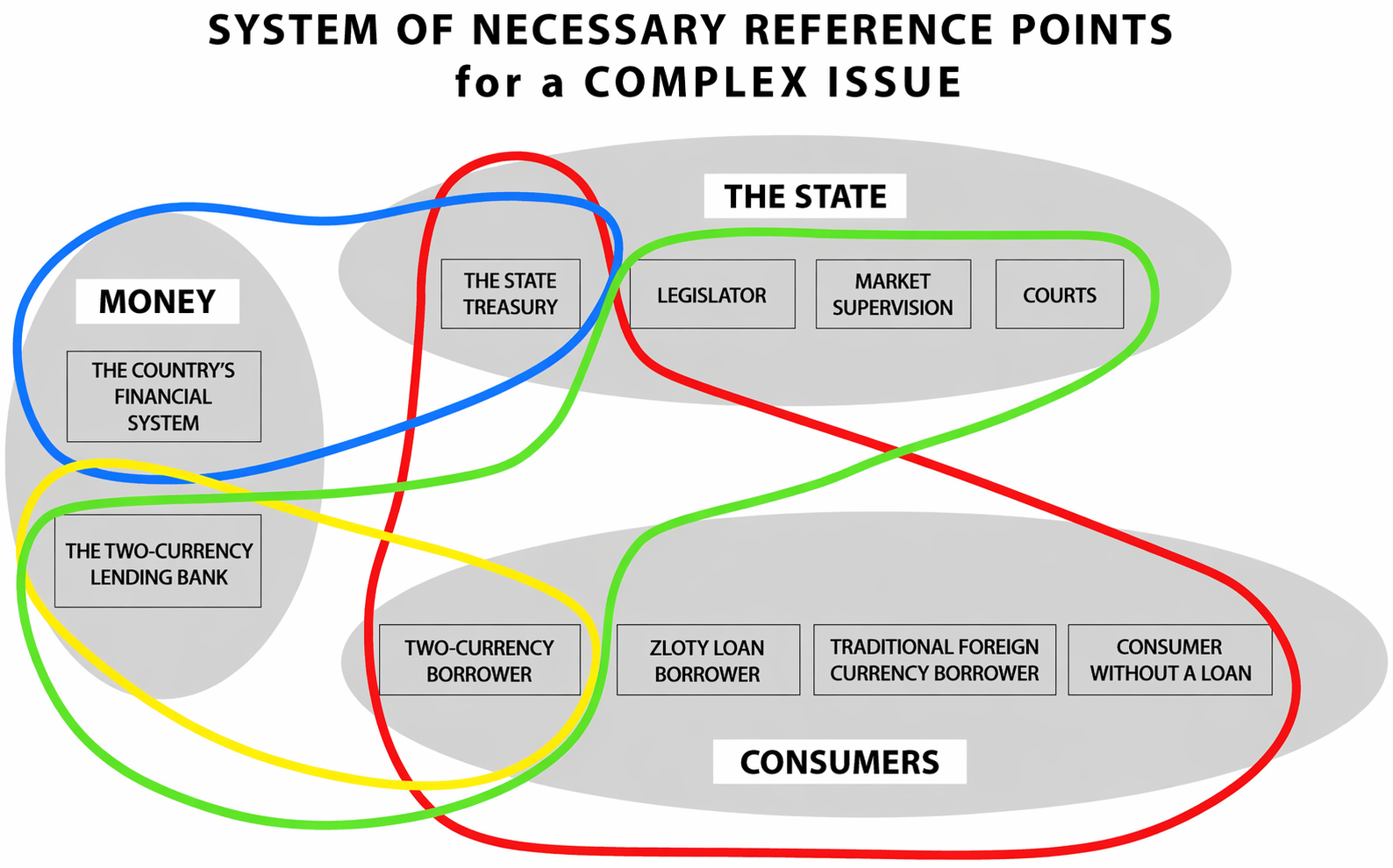

System of Reference Points

– it shows the most important perspectives from which this problem is viewed in public discourse.

I grouped them into three categories.

Description of the diagram:

Within the System of Necessary Reference Points, I distinguished ten reference points grouped into three categories:

A/ CONSUMER → 1) Dual-currency borrower, 2) PLN borrower, 3) Classic foreign-currency borrower, 4) Consumer without a loan,

B/ STATE → 5) Legislator, 6) Market supervision, 7) Courts, 8) State Treasury,

C/ MONEY → 9) The country’s financial system, 10) The dual-currency lending bank.

I marked four relationships between the individual Reference Points with different colors.

The yellow line represents the relationship between the LENDING BANK and the dual-currency CONSUMER-BORROWER.

For these two Reference Points, explaining the problem of dual-currency loans is the most important, because it will directly affect their future existence.

CONSUMER as a Reference Point has four variants. A consumer who has taken out a dual-currency loan is in a different situation from a PLN BORROWER, a CLASSIC FOREIGN-CURRENCY BORROWER, and a CONSUMER WITHOUT A LOAN, because they all have no direct interest in solving this problem, but they do have an indirect interest—they use the services of corporations, which means they must enter into agreements with entities that have a much stronger negotiating position, and therefore they should be protected by state institutions.

In addition, in public discourse there are arguments about the unfairness of court judgments declaring dual-currency loans invalid in relation to PLN borrowers and classic foreign-currency borrowers, and so the validity of those arguments should be examined.

There is also a second relationship connecting all consumers (marked with a red line): as citizens, they all contribute their money to the State Treasury, while on the other hand the state is obliged to use that money to ensure safe existence for all citizens, and even assistance when needed.

STATE – in the case of this Reference Point – also has at least four embodiments.

Three embodiments (green line) concern the legal order that the state establishes, which among other things should guarantee consumer protection in transactions with corporations: law-making – the LEGISLATOR, MARKET SUPERVISION – which may consist of various institutions (e.g. UOKiK, the Financial Ombudsman), and the JUDICIARY, that is, ensuring the real possibility for every citizen to pursue justice.

The fourth embodiment of the state concerns economics – the relevant state authorities must supervise the country’s financial system (blue line), and in the event of serious danger rescue it using funds accumulated by the STATE TREASURY.

The last reference point is, broadly speaking, MONEY. Banks operate within the financial system, which is why the condition of banks granting dual-currency loans may affect the condition of the country’s entire financial system, and thus also the economic situation of all its citizens.

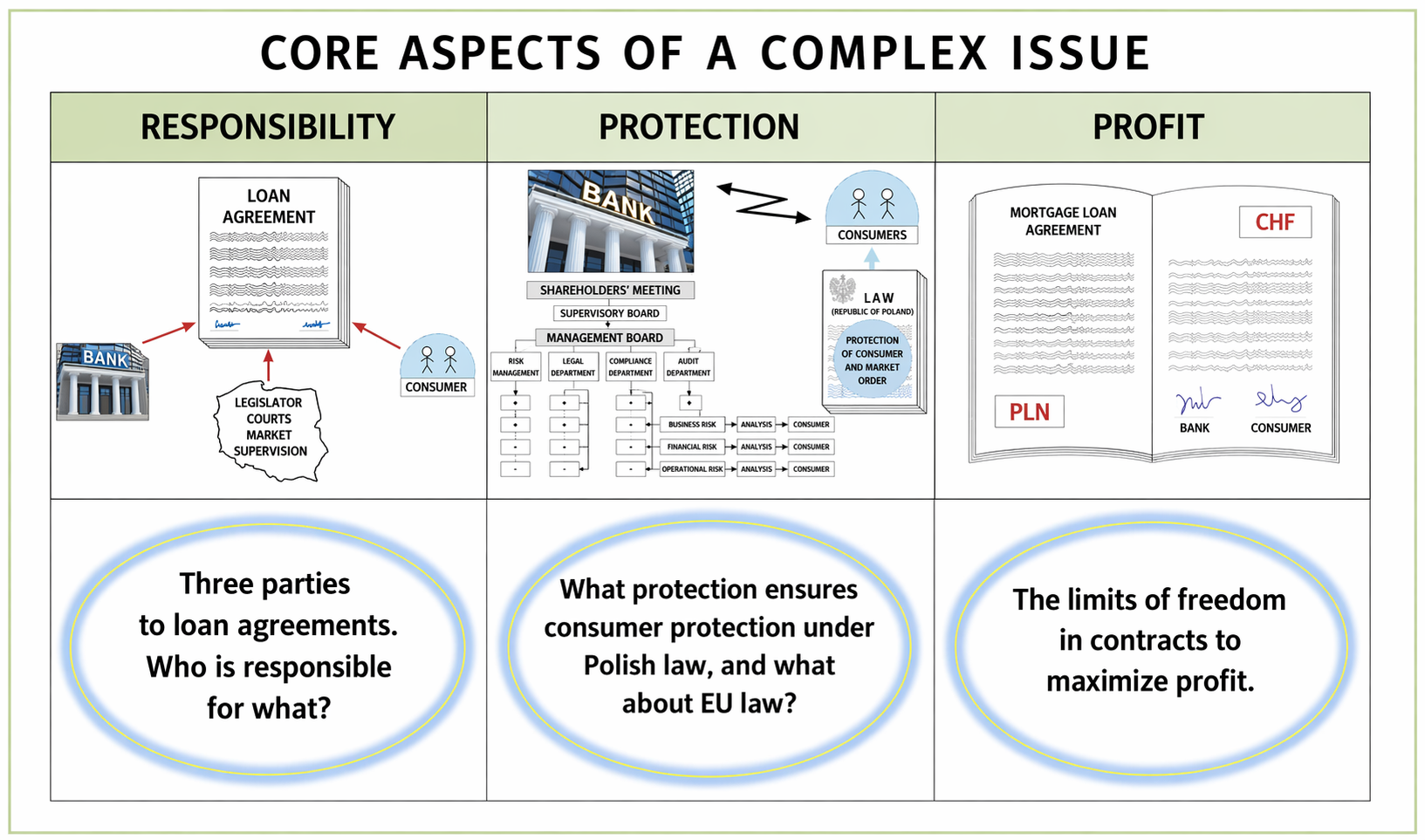

Three Core Aspects

– they define the main areas in which the public discourse concerning dual-currency loans takes place.

Description of the table:

The way in which I defined the CORE ASPECTS is not the only possible one, because they can be named in different ways.

For example, they may be defined as scientific disciplines – instead of my classification:

PROTECTION-RESPONSIBILITY-PROFIT – one could say LAW-PSYCHOLOGY-ECONOMICS, or ORDER-TRUTH-MONEY. A classification referring to scientific disciplines might seem more solid, but it would also be misleading, because the issue does not fit only within those three scientific disciplines.

Regardless of the naming, however, I determined that there are three main areas of discourse surrounding this topic.

Of course, each aspect should be analyzed and developed by scholars from several scientific disciplines, but up to this point I had to do everything alone.

Therefore, I developed only Core Aspect-1 on a preliminary basis: the invalidity of the loan agreement.

Within it, I analyze the following issues:

– the legal correctness of the dual-currency loan agreement;

– the comprehensibility of the consequences arising from the text of this agreement, in other words, the readability of the agreement;

– who bears responsibility for introducing dual-currency agreements into circulation;

What did I develop as part of the example?

In order to demonstrate

what Integrated Information on dual-currency loans

could look like, I designed its structure and developed one segment of it from beginning to end.

MAP OF THE ACTIVE PART OF INTEGRATED INFORMATION

ON DUAL-CURRENCY LOANS

As can be seen in the graphic, the red active elements constitute only part of the integrated information.

My example IAI model is intended to show how to develop a Complex Issue so that it presents the problem in accordance with the principles of Broad Synthetic Truth, and how to highlight important data thanks to which anyone – regardless of their prior knowledge – will be able to analyze it logically.

An important element in the structure of Integrated Information is the Synthesis Blocks, that is, the idea of arranging the necessary information in such a way that it forms a coherent and logical whole. No currently available source of information provides data arranged in this way.

I carried out several comprehensive analyses on materials concerning CI1.

They are presented in the Analytical Issue AI-1, as Analytical Layers [from AL-1 to AL-8].

I concluded two of them with the development of synthesis blocks:

AL-1 – the currency of the loan,

AL-8 – the structure of the dual-currency loan agreement → is this agreement a comprehensible message for the average consumer?

These are two important issues – personally I consider them crucial – for the topic of dual-currency loans, but of course they are only the tip of the iceberg.

To sum up – the most important thing here is the idea of an active internet information structure and the construction of its model.

A complete development of the complex issue of pseudo-Swiss-franc loans was not my intention.